Machine Learning and Investing: Forecasting Fundamentals w/ Ensembles

Machine Learning and Investing: Forecasting Fundamentals due west/ Ensembles

Quantitative factor portfolios generally use historical company key information in portfolio construction. The primal assumption behind this approach is that by fundamentals proxy for elements of risk and/or systematic mispricing. However, what if we could forecast fundamentals, with a pocket-size margin of error, and compare that with market expectations? Intuitively, this seems like a more promising approach. I explore this concept using all-time practices from the scientific discipline of forecasting and machine learning techniques, namely Random Forests and Gradient Boosting. The goal of this research is to build a value composite model based on forecasted fundamentals to price and come across how this works relative to the "old" method of using historical fundamentals to price. My approach is as follows:

I apply the in-sample data to train the models to predict forward-looking earnings, free cash menstruum, EBITDA, and Net Operating Profit After Taxes.

I use these forecasts to build a value portfolio that seeks to improve upon traditional, less sophisticated value approaches.

Lesser line? The combined value portfolio out of sample did not produce statistically significant outperformance versus the equal weight portfolio (as a comparing to the long-only value composite) or versus greenbacks (for the long/short portfolio).(1)

Groundwork

Forecasting as a scientific discipline has adult over the past decades with the use of standard statistical techniques, such as a multiple linear regression, to more than advanced auto learning techniques. Some of the best practices or ideas evidenced by inquiry are every bit follows:

Crowds can ofttimes arrive at a superior and more robust estimate than the best private forecast under the right circumstances

Using an ensemble of methods and approaches is oft superior to a single arroyo

Start with the base example (exterior view) and piece of work into the inside view (the nuances of the specific case)

With investing in equities at that place has been a prime focus on earnings (net income) projections as a proxy for sustainable company cash flow, which is the core input in a discounted greenbacks flow valuation (DCF) for company valuation. In the quantitative investment domain, the information used for portfolio construction has primarily been bodily historical data (e.g. Fama & French and AQR) to build portfolios based on specific metrics, such as the near well-known Marketplace Value/Book Value ratio for the value factor. On the discretionary side of nugget management there has been more of a focus on the predictable future of the economy and company profits, with the prize going to the superior analyst who tin forecast ameliorate than the remainder. A natural curiosity: What if we combined the best practices of forecasting and motorcar learning, and so created a quantitative equity portfolio of the companies with the best forecasted earnings in relation to their electric current nugget toll?

The Crystal Ball Portfolio

What is the portfolio functioning if one could know in advance the next 12-month company fundamentals?(2) I constructed this ideal Crystal Brawl portfolio in the aforementioned way as the Random Forest model. The Cheap portfolio is the cheapest 50% of stocks and the Expensive portfolio is the bottom 50% of stocks based on a composite valuation score from the post-obit four factors:

Price to 12 months forward 12 calendar month abaft earnings

12 months forward 12-month abaft Return on Invested Capital

Enterprise Value to 12 months forward 12 calendar month trailing EBITDA

Each factor is winsorized at the 90% level to prevent the undue influence of outliers. Next the cistron values are given a Z score, and the terminal Valuations score is the sum of the four Z scores. The portfolio has 4 tranches that each rebalance annually but individual tranches rebalance on subsequent quarter periods to minimize timing luck (Hoffstein, 2019). Tranches trade iii months after the earnings date, to eliminate wait-alee bias, but is irrelevant in this example. For example, tranche 1 would trade the information from Q3 2000 at the end of Q4, since there is by and large a i to iii-month lag in earnings reports.

The results are hypothetical results and are Non an indicator of future results and practice NOT represent returns that any investor really attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest straight in an index.

The results are hypothetical results and are NOT an indicator of future results and practice Not represent returns that whatever investor actually attained. Indexes are unmanaged, do not reverberate management or trading fees, and ane cannot invest straight in an index.

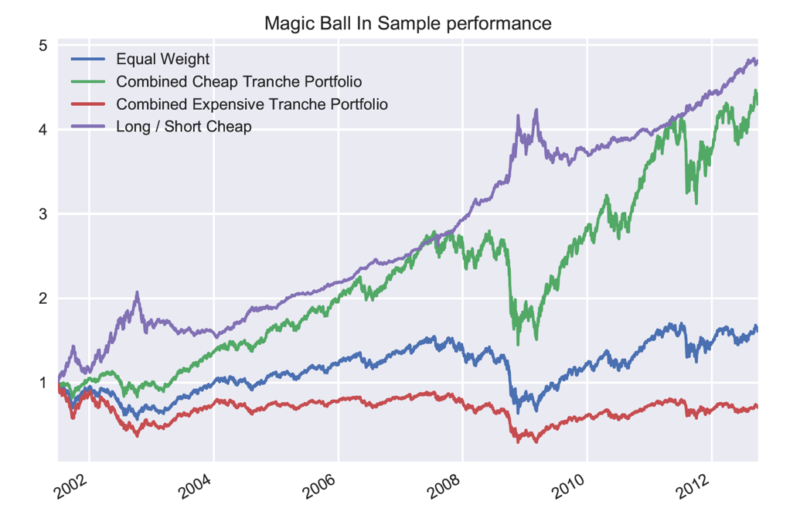

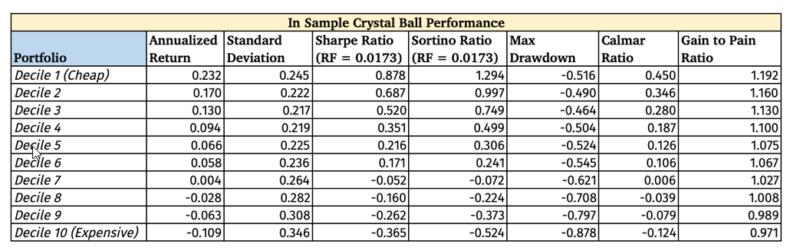

Below is the in-sample Crystal Ball Portfolios by Decile, where yous tin can encounter the not bad adventure and return differences. For obvious reasons, the portfolio Z scores were not winsorized in the below decile data.

The results are hypothetical results and are Non an indicator of hereafter results and do NOT stand for returns that any investor actually attained. Indexes are unmanaged, exercise not reflect management or trading fees, and 1 cannot invest straight in an index.

Equally to exist expected, there is a loftier performance dispersion between deciles, and a rima oris-watering Long/Short Sharpe Ratio of 1.28. But the results are designed to be unrealistic. The main take away is that if we can reliably forecast the hereafter fundamentals we can construct high return to risk portfolios.

Relevant Literature

Tetlock and Gardner (2016) have gleaned principles of superior forecasters. Superior forecasters start with a focus on the base case, or outside view (Kahneman (2015)), which is how a situation historically has transpired. After a reliable base of operations case guess is derived, and so the unique details of the present state of affairs are factored in to adjust the base of operations case probability. Start with the historical pattern and arrange for the present. (related to Bayesian inference, discussed hither with an awarding to investing.) According to Surowiecki (2014), in gild for crowds to accept wisdom beyond any individual participant, they need to have the post-obit characteristics:

Independent

Diversified

Decentralized

Take a pricing or voting mechanism equally a mode to aggregate data

For the above to atomic number 82 to a good estimate from the crowd, the errors must be random and not systematically biased. This can oft be untrue for asset markets considering of the bias against brusk selling (potentially a non-result for the futures market place) and during bubbles/crashes the errors are biased towards the bull or bear case. Tetlock and Gardner (2016) mention that superior forecasters know when in that location is madness of the crowds as well as wisdom of the crowds.

Machine Learning for Future Company Fundamentals

Alberg and Lipton (2017) used a deep neural network to form portfolios based on forecasted futurity fundamentals and saw a 2.seven% annualized alpha vs. a standard gene based portfolio. They used data from Compustat starting in 1970, which provided a far greater number of data points to train their machine learning model vs. Sharadar'southward data that starts in 1999. Shiller (1980) mentioned how stocks motility more than than they should if the price of a stock was the best predictor of future dividends. Thus, in that location is a high noise-to-signal ratio for individual stock prices, only I assume there is a lower noise-to-signal ratio with company fundamentals due to the greater stability and lower variance of fundamental data from one quarter to the next. Moreover, with the large number of unlike types of agents in the stock marketplace with different motivations information technology will exist hard to tease out singular causes backside stock cost movements. There has been inquiry conducted using machine learning techniques around portfolio construction and hazard assessment (see De Prado, 2016 and Zatloukal, 2019), but not much on creating portfolios based on forecasted company fundamentals.

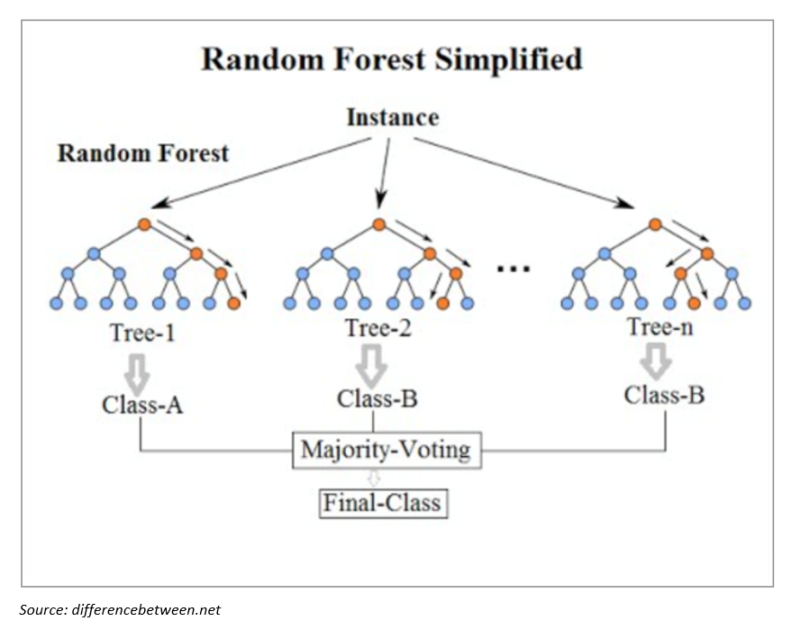

Random Forests — An Introduction

Random Forests is a supervised auto learning technique that uses a composite of decision copse to make a forecast.(three) The Random Forests tin be used equally a classification (e.g. volition the price of the stock go up or down) and as a regression function (i.e. what will the earnings be next quarter?) The researcher chooses the hyper parameters that the Random Forests uses to create the decision trees. The main hyper parameters for Random Forests are the number of Forests to create, the maximum depth of each forest, and the number of random features to use in each forest for splitting the conclusion tree.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that whatever investor actually attained. Indexes are unmanaged, do non reflect management or trading fees, and one cannot invest directly in an index.

Random Forests utilize the wisdom of crowds, namely that "a large number of relatively uncorrelated models (trees) operating as a committee will outperform any of the individual constituent models" (Yiu, 2019). Uncorrelated models combined can practice well since "the trees protect each other from their individual errors (equally long as they don't constantly all err in the same direction)" (Yiu, 2019). The uncorrelated errors can cancel each other out and allow the signal to emerge. Random Forests apply Bootstrap Assemblage, where a random sample (with replacement) of the grooming data is used to construct a decision tree. Moreover, a random set of features is used to split the determination tree. This added randomness aims to minimize variance and overfitting (Yiu, 2019). The terminal decision tree is an average of all the created forests (Burkov, 2019). The Random Forest Regressor Function from Python'south Scikit-Larn Auto Learning parcel was used for the research with the following parameters:

n_estimators = 1000

random_state = 42

criterion = "mse"

max_depth = None

max_features = 16 (1/3 of feature fix)

Information

US Equity price and fundamental data is from Sharadar, and has all listed and delisted US traded equities from 1999 up until the present. The in-sample data is from January ist 1999 until the 31st of December 2012, of which the about recent 25% of the in-sample data is used as a validation set. The out-of-sample data is from Jan 1st, 2013 to September 30thursday 2019. Transactions costs, taxes, and slippage are ignored.

Quantitative Process and Rationale (Methodology)

The overall objective is to predict the next 12 months of earnings, net operating profit later on taxes (NOPAT, used in ROIC calculation), free cash flow, and earnings before interest, revenue enhancement, depreciation, and amortization (EBITDA) for United states of america-traded companies using a Random Forests model. Assuming the model is accurate, rank stocks based on electric current cost to forecasted fundamentals and invest in the cheapest l% (long only) and/or short the nearly expensive (50%). I constrained the data set to simply Usa domiciled equities (listed and delisted). I isolated each equity sector for grooming the Random Forest model with the supposition that a more homogenous group of companies, i.e. a specific sector, would have more easily discernable drivers to sales and earnings. My features are broken down into two categories: Economical and Visitor Specific Fundamentals. The economic features were chosen to capture the overall economical environment, with many shown to have predictive power over future economical contractions, such as the yield curve (Estrella, 1996), and would hopefully reveal whether the economic environs was conducive to company profits. Economic Features (Source: St. Louis FRED and Constitute for Supply Chain Management):

Consumer Cost Inflation (CPI)

Core CPI

West Texas Intermediate Oil Price

Price of Gold

ten Year Treasury Yield

3 Month Treasury Yield

10 Yr – iii Month Yield spread

3 Month LIBOR (USD)

High Yield Pick Adapted Spread

Investment Course A Choice Adjusted Spread

High Yield OAS – Inv. Grade A OAS (Credit spread)

Dollar Index

Unemployment Rate

Real Personal Consumption

Building Permits

Wilshire 5000 Index

ISM Manufacturing PMI Index

TED Spread

Company Fundamentals (source: Sharadar, calculations my own):

Revenue

Uppercase Expenditure

Debt to Disinterestedness

Earnings Before Income Tax, Depreciation, and Amortization (EBITDA)

Operating Income

Revenue enhancement Expense

Gross Profit

Research and Evolution

Selling and General Administration Expense

Interest Expense

Return on Invested Capital letter

Return on Disinterestedness

Enterprise Valued to EBITDA

Electric current Debt

Not-Current Debt

Deferred Revenue

Depreciation and Amortization

Inventory

Nugget Turnover

Working Majuscule

Capital letter Expenditures to Sales

Year on Year Revenue Growth

Year on Yr Net Income Growth

Year on Year Internet Cash Flow from Operations Growth

Sector Year on Year Cyberspace Income Average

Ratio of Company vs. Sector Twelvemonth on Twelvemonth Net Income Growth

This feature was chosen to mensurate the base case growth for the manufacture with the assumption if the company was doing exceptionally well there was likely a reversion to the mean potentially in the futurity

Sector Yr on Year Revenue Average

Ratio of Company vs. Sector Year on Year Acquirement Growth

Earnings Accrual Ratio

I included all companies that had a market capitalization of $1 billion or more based on the previous quarter in order to minimize liquidity issues in trade execution. After the Random Forests model was trained, the model predicted the forwards 12 month earnings, EBITDA, NOPAT, and complimentary cash flow for each company. Notation that there was a Random Forests model for each of the 4 factors and for each sector, resulting in 44 Random Forests models. From at that place, the portfolio would exist constructed by going Long the cheapest fifty% of companies (lower toll to forecasted earnings, for instance) and short the most expensive 50% of companies. The 4 key factors:

Render on Invested Majuscule

Cost to Earnings

Cost to Free Cash Period

Enterprise Value to Earnings Before Interest, Tax, Depreciation, and Amortization (EBITDA)

Each gene is winsorized at the 90% level to prevent the undue influence of outliers Adjacent the factor values are given a Z score, and the concluding Valuations score is the sum of the iv Z scores. The portfolio has 4 tranches that each rebalance annually but start on subsequent quarter periods. I have utilized the staggered portfolio tranche limerick to avoid timing luck in the rebalancing dates. The tranches merchandise 3 months afterwards the earnings date to eliminate wait-alee bias. For case, tranche one would trade the data from Q3 2000 at the stop of Q4, since there is generally a 1 to three calendar month lag in company central reports. The combined portfolio merely uses the dates when all 4 tranches are active and invested. Each Sector would accept their unique value portfolio. Then all eleven sector portfolios are combined equal weight to create the overall Value portfolio.

Descriptive Statistics

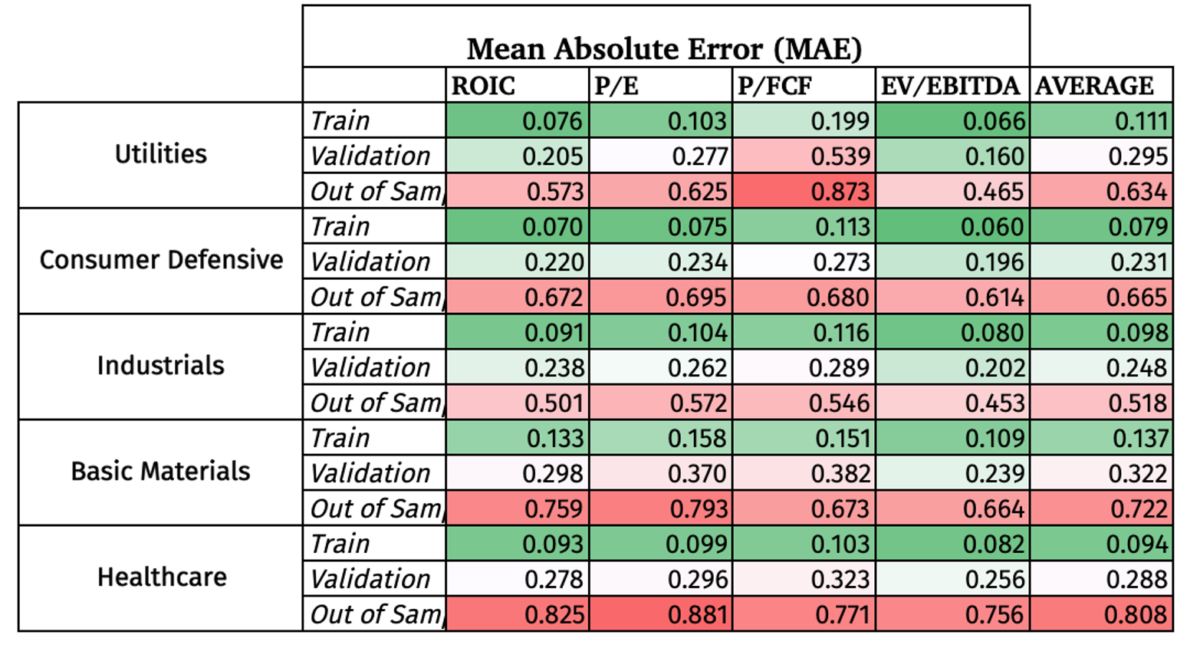

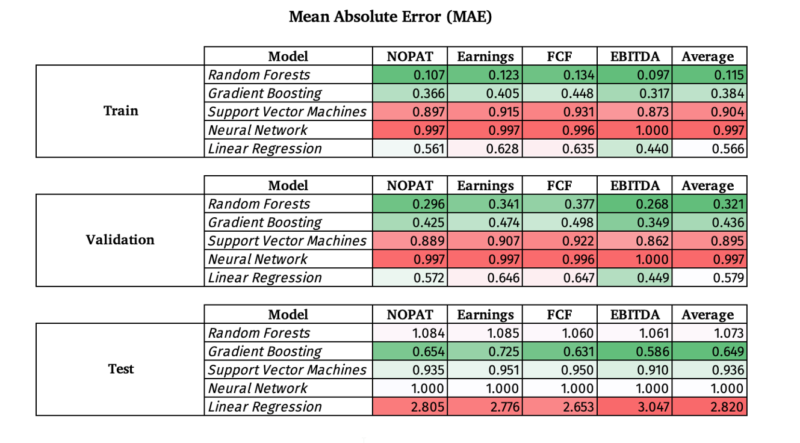

The Mean Accented Error measures the accented percentage difference between the Random Woods forecast and the actual data, with lower being improve. It is a common metric to examination the accuracy of a car learning regression model.

The in sample has the lowest MAE by pattern, and the validation set increased slightly. Merely the big surprise is how loftier the MAE was in the Out of Sample data. I have colored coded the results to make information technology easier to see the contrast.

The results are hypothetical results and are NOT an indicator of future results and exercise Not stand for returns that any investor actually attained. Indexes are unmanaged, practice not reflect direction or trading fees, and one cannot invest straight in an index.

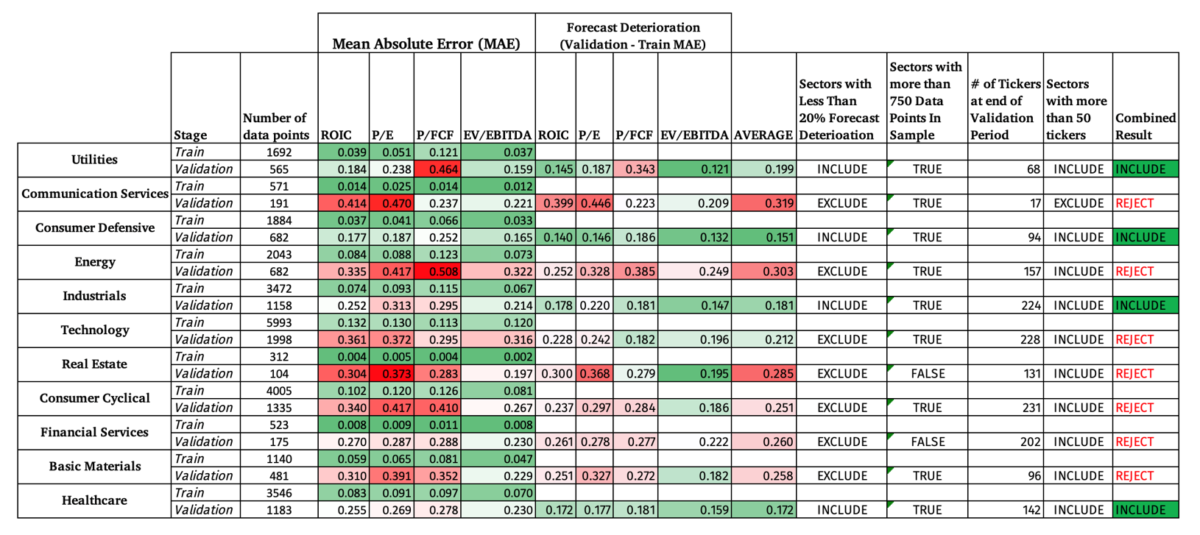

After testing the strategy in-sample (railroad train vs. validation), the eleven sectors were narrowed downwards to those sectors that meet all 3 criteria:

At least 50 companies at the end of the in-sample time catamenia

More than 750 data points to railroad train the model

Less than 20% deterioration in the MAE from in-sample to validation.

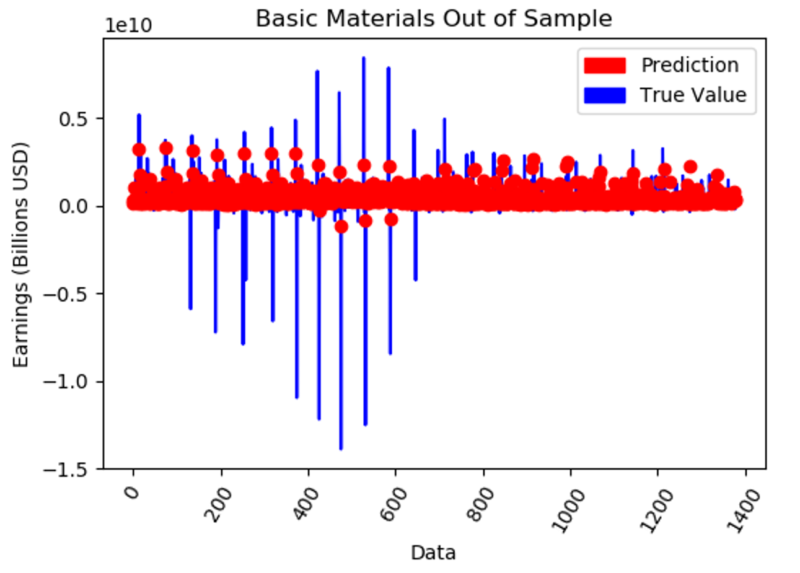

This resulted in choosing only 5 sectors, namely, Utilities, Consumer Defensive, Industrials, Basic Materials, and Healthcare. Too the obvious deterioration in the MAE out of sample, the model did the all-time job at accurately forecasting EBITDA compared to the other 3 metrics, merely with still a high MAE.

The results are hypothetical results and are Non an indicator of futurity results and do Non represent returns that any investor actually attained. Indexes are unmanaged, do not reflect direction or trading fees, and 1 cannot invest directly in an index.

Here is an example of what is looks like to have such a high MAE out of Sample.

The results are hypothetical results and are NOT an indicator of time to come results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, practise non reflect direction or trading fees, and i cannot invest directly in an index.

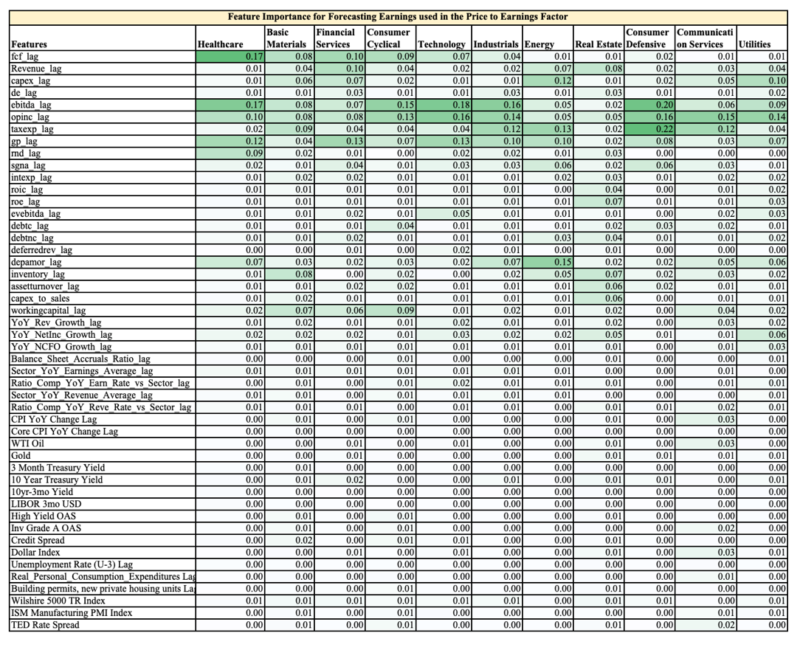

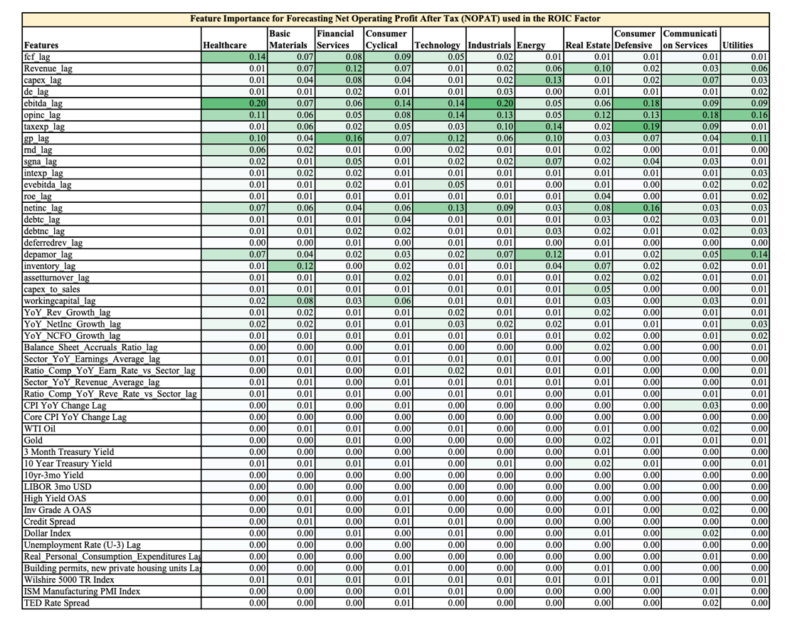

Below is a table showing the relative feature importance (0.17 = 17% out of 100%) in the final Random Forests Model for each sector, highlighted to provide easier digestion of the numbers. The first 30 features are visitor central information and the rest are macro-economical information. You can easily run across 2 observations:

The company key data is far more than important than the overall macro environment when information technology comes to forecasting future earnings

Each sector has different ranking of feature importance, hence the value of preparation the Random Forests models on each sector vs. on the overall market.

Every bit an aside, a discretionary annotator could use this feature importance to help them focus on the most influential variables when forecasting company fundamentals.

The results are hypothetical results and are Not an indicator of future results and do Not stand for returns that any investor really attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest direct in an index.

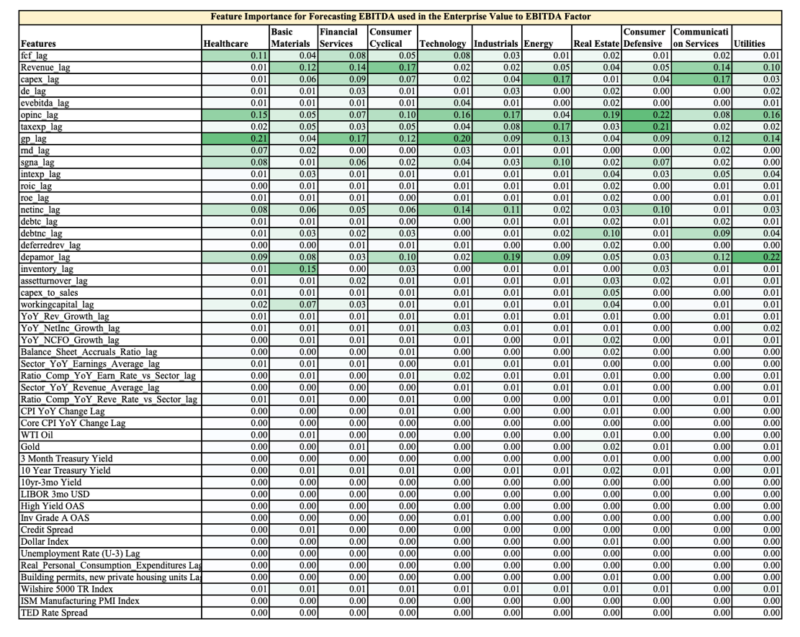

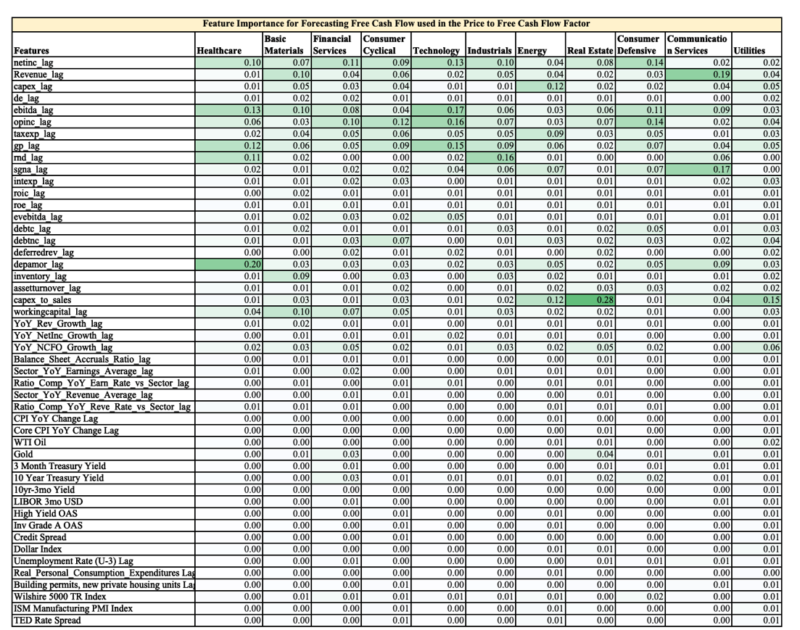

The appendix has the feature importance for Toll to Free Greenbacks Flow, Enterprise Value to EBITDA, and ROIC.

The results are hypothetical results and are Not an indicator of futurity results and exercise NOT represent returns that any investor really attained. Indexes are unmanaged, exercise not reflect management or trading fees, and 1 cannot invest direct in an index.

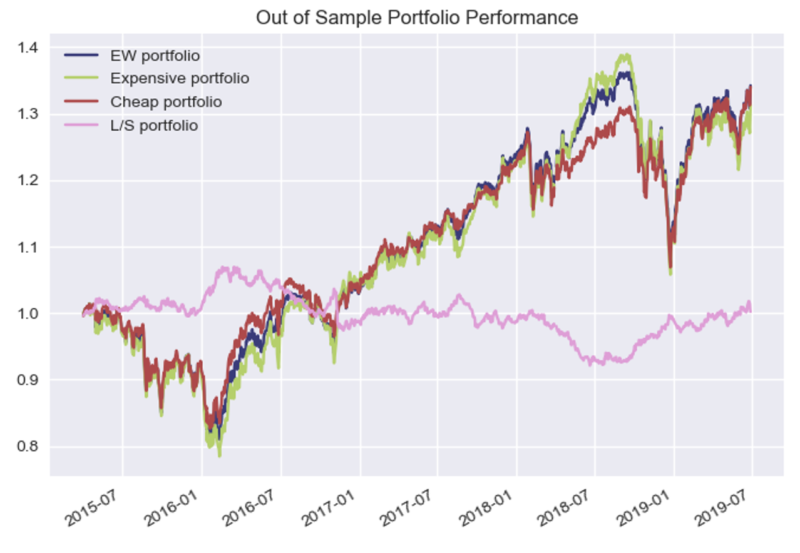

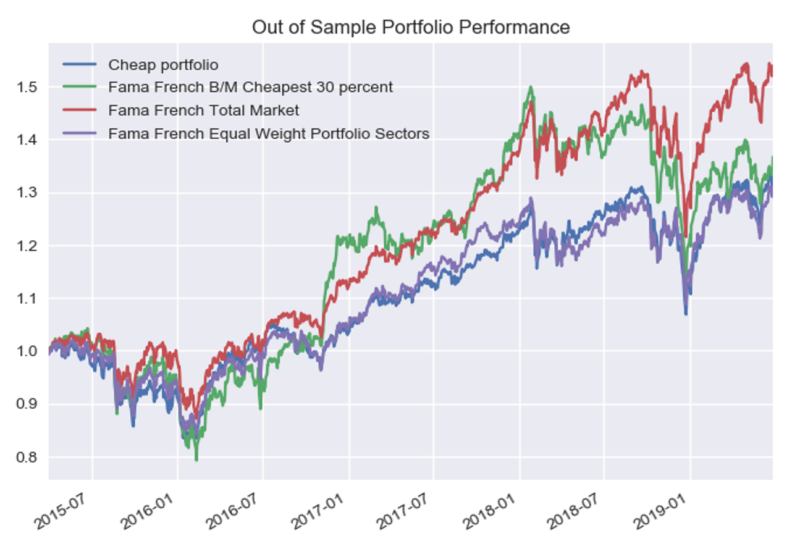

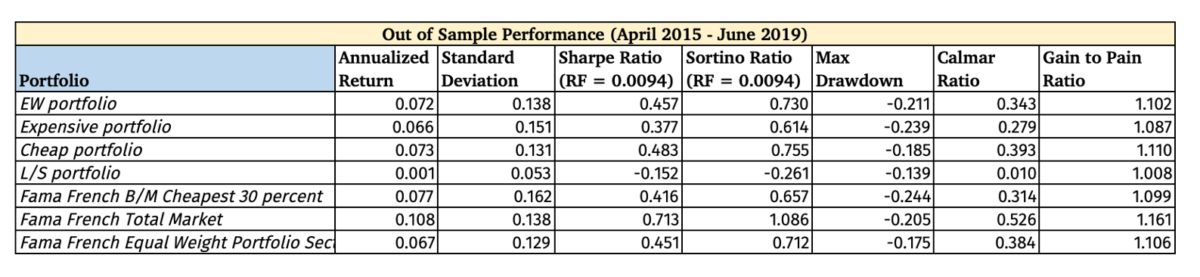

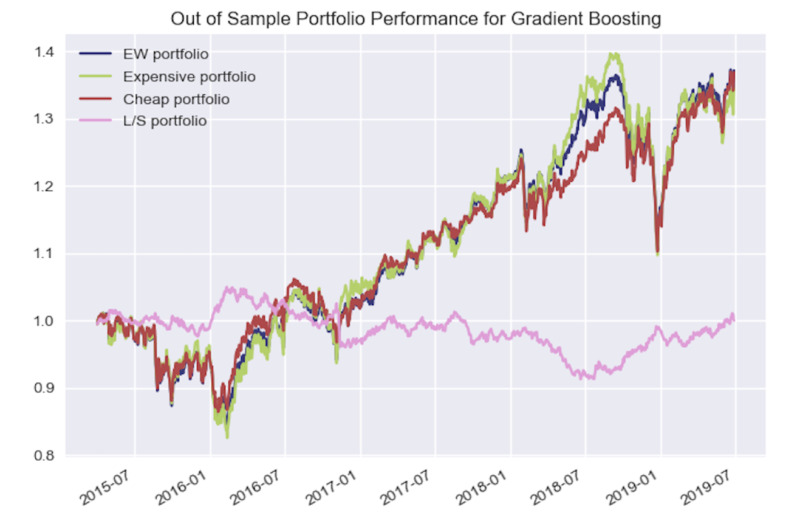

Nil remarkable stands out from the operation chart above, except the slight outperformance and underperformance of the Long-Short portfolio in 2016 and 2018 respectively. Note that even though the out of sample fundamental start in Q1 of 2013, information technology takes five quarters to get Year on Twelvemonth feature data, ane quarter of lag fourth dimension in trade execution, and 3 quarters to have data for all 4 tranches, thus the first combined portfolio data starts in April 2015 (Q2). Now vs. Fama French Total Market Data:

B/M Cheapest – the cheapest 30% of USA traded companies based on Book to Market

Full Market – Market Cap weighted total market value

Equal Weight Portfolio Sectors – 20% in each of the 5 sectors used in Out of Sample Portfolio test to effort to compare apples to apples

The results are hypothetical results and are NOT an indicator of future results and do Not represent returns that whatsoever investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an alphabetize.

The large performance discrepancy in a higher place for the Total Market index is driven in part past the allotment to Technology, which was not included in the RF model.

The results are hypothetical results and are NOT an indicator of time to come results and do Non represent returns that whatsoever investor actually attained. Indexes are unmanaged, exercise non reflect management or trading fees, and one cannot invest directly in an index.

Statistical Significance of Findings

The Long but and Long-Short portfolio did not generate a high t-stat to arrive statistically meaning at the 5% level.

The results are hypothetical results and are NOT an indicator of future results and do Not represent returns that whatever investor really attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index.

Assay of Findings

Why was there such lackluster performance in the Random Forest's ability to forecast future fundamentals? Looking at the R^2 score (table beneath), shows that the Random Forests Model, going from the train to validation to test information gear up, explains less and less of the actual time to come fundamental values (i.e. actual earnings) which is to exist expected to some extent.

The results are hypothetical results and are Non an indicator of time to come results and practise NOT represent returns that whatsoever investor really attained. Indexes are unmanaged, do not reverberate management or trading fees, and one cannot invest direct in an alphabetize.

Moreover, as shown previously, the Mean Absolute Error Percentage increases significantly from the train to validation to the test data. In essence, the model did not do a adept job forecasting future fundamentals. This tin mean a few things:

The Random Forests Model with this data set, regardless of whatsoever additional features added to the feature ready, could not predict accurately enough the future visitor fundamentals to create alpha

Another machine learning model could have produced blastoff with this dataset (we will look at Gradient Boosting later on in the mail service).

There are qualitative (i.due east. How potent is the moat of the company?) or hard to quantify factors that determine the future fundamentals of a company that were not a part of the model

A systematic and quantitative machine learning model won't work across a sector and each company will demand more customizable forecasts.

Mean Absolute Mistake for Other Models

How practice other ML models piece of work in general vs. Random Forests? Below are three other models combined with a simple linear regression model. The post-obit ML models and their respective Scikit-acquire part:

Random Forests – sklearn.ensemble.RandomForestRegressor

Linear Regression – sklearn.linear_model.LinearRegression

I kept the hyper parameters in accordance with their default values and did non tune the hyper parameters. Moreover, I used all companies and sectors with a market place cap of $ane billion or more and did not railroad train a unique model on each sector.

The results are hypothetical results and are Non an indicator of future results and do NOT correspond returns that any investor actually attained. Indexes are unmanaged, do non reverberate management or trading fees, and one cannot invest directly in an index.

A few observations:

EBITDA continues to be the easiest to predict out of sample (test) compared to the iii other fundamental factors, which makes sense since information technology is the "highest" on the income argument and requires the least number of steps to arrive at from acquirement. I would postulate that revenue would be the easiest to predict.

The Linear Regression model had the greatest over fit, followed by the Random Forests model when looking at how the railroad train, validation, and test MAE changed

It is interesting to see that the Support Vector Machines (SVM) had roughly the same MAE for railroad train, validation, and test, although it was quite loftier effectually .90

Slope Boosting essentially beat the Random Forests model out of sample.

The Neural Network Model was essentially a random guess and added no value at all with an approximate i.00 MAE fifty-fifty with Train and Validation sets

The general Random Wood model, which trained and tested on all companies had an average MAE of 1.073 out of sample, merely had an average MAE of .6694 on the five sectors (Utilities, Consumer Defensive, Industrials, Basic Materials, Healthcare) on average beyond all four fundamental factors out of sample. By implication, if the Slope Boosting model was trained on each sector by themselves and their hyper parameters were tuned using the validation data gear up, it likely the MAE out of sample for the Gradient Boosting model would be fifty-fifty lower.

Hindsight "Out of Sample" Portfolio Performance

While committing a research felony by testing more than once on the out of sample dataset, out of curiosity, how would the Slope Boosted (GB) model accept work in portfolio structure? The GB model plainly did a better job in general on out of sample prediction. If nosotros come to notice that the GB model generates alpha we would need to exist very stringent by using a Deflated Sharpe Ratio (Bailey, 2014) or very high statistical significance level (i.e. 99% or higher) to tease out luck. Both Random Forests and Gradient Boosting are composed of decision copse. The two master differences (Glen, 2019) are as follows:

How copse are built: random forests build each tree independently while slope boosting builds one tree at a time. This additive model (ensemble) works in a forrard phase-wise manner, introducing a weak learner to better the shortcomings of existing weak learners.

Combining results: random forests combine results at the end of the procedure (by averaging or "bulk rules") while slope boosting combines results along the way.

The Gradient Boosting Regressor Function from Python's Scikit-Acquire Automobile Learning bundle was used for the research with the following parameters tuned after cross-validation:

n_estimators = 3000

random_state = 42

min_samples_split = 2

max_depth = iv

learning_rate= .01

loss = 'ls'

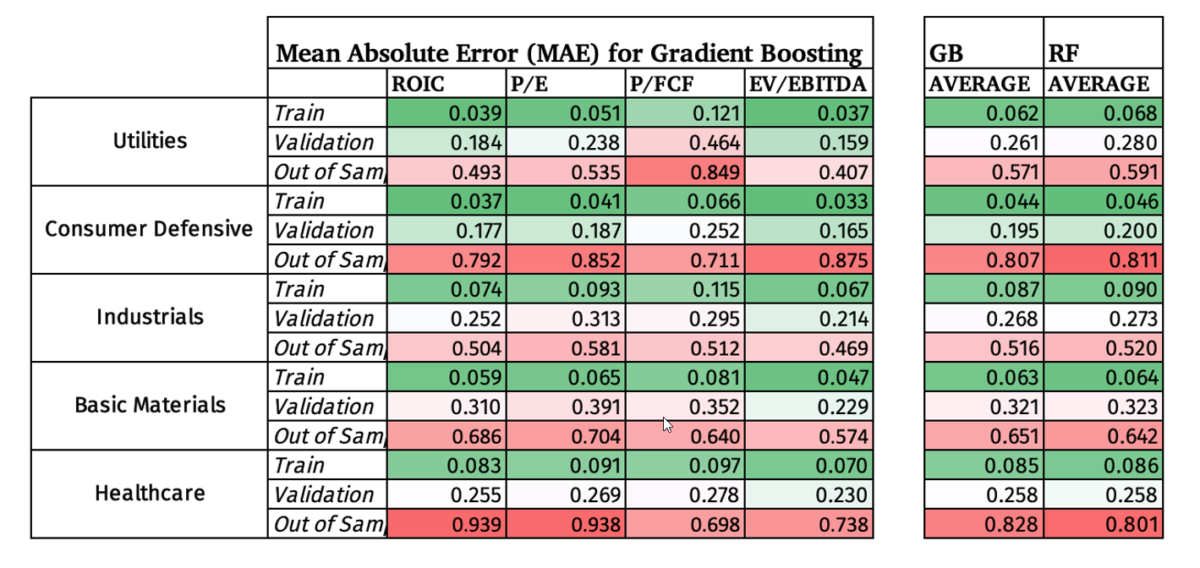

Beneath we accept the same MAE format as with the Random Forests model, but this time Basic Materials didn't make the cut off.

The results are hypothetical results and are Not an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do non reflect management or trading fees, and ane cannot invest directly in an index.

Beneath are the MAE percentages for all five sectors included in the Out of Sample Random Forests Model for comparison:

The results are hypothetical results and are Non an indicator of futurity results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, practise not reflect direction or trading fees, and i cannot invest directly in an index.

We tin see that the Gradient Boosting model did not produce, on average, superior predictions compared to the Random Forests model, which is to some extent surprising since the full general GB model did significantly amend out of sample than the RF model. All the same, since GB and RF are both ensemble models that employ decision copse information technology is understandable that they would create very similar results. Nosotros run across beneath a very like and unimpressive operation for the GB model as with the RF model.

The results are hypothetical results and are NOT an indicator of futurity results and exercise NOT represent returns that any investor actually attained. Indexes are unmanaged, practise not reflect direction or trading fees, and i cannot invest directly in an index.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that whatever investor actually attained. Indexes are unmanaged, practise not reflect management or trading fees, and one cannot invest straight in an index.

Farther Research and Decision

In conclusion, the Random Forests and Gradient Boosting motorcar learning models did not produce statistically meaning outperformance, which is primarily driven past their high Hateful Accented Error Percentages. In other words, the machine learning models had high variance and weren't very authentic in their ability to predict future company fundamental values. A good comparison would be to see if Wall Street Analysts on average do a ameliorate job at predicting future fundamentals vs. the Random Forests model, which could be done using Zach's Consensus Earnings Approximate History Database. Moreover, I would await the model to take performed meliorate out of sample if I had access to the Compustat and CRSP data which would extend the data by around 37 years (back to 1963). With access to those databases you could apply deep learning and other unsupervised techniques which require larger datasets than the one I had access to with Sharadar. Another interesting concept to explore further would be around the idea of the range of accuracy needed in forecasting fundamentals to achieve alpha. Specifically, what level of Hateful Absolute Mistake Pct does a manager or analyst need when forecasting earnings, for case, to attain blastoff? Could an investor vanquish the market with even 30% MAE, meaning that they accept a xxx% banding of accuracy on the positive and negative side of bodily fundamentals? If we could know the minimum skill required in forecasting, an annotator could humbly review their record and determine if they have what information technology takes. This could shed calorie-free on how good is proficient enough. Please reach out if you accept ideas on how to improve this research.

Appendix

Characteristic Importance Ranking for NOPAT used in calculating ROIC

The results are hypothetical results and are Non an indicator of futurity results and do NOT stand for returns that whatever investor really attained. Indexes are unmanaged, do not reflect management or trading fees, and ane cannot invest directly in an alphabetize.

Feature Importance Ranking for EBITDA used in EV/EBITDA

The results are hypothetical results and are NOT an indicator of hereafter results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, practise not reverberate management or trading fees, and one cannot invest directly in an alphabetize.

Feature Importance Ranking for Free Cash Flow used in Price / Costless Greenbacks Flow

The results are hypothetical results and are Not an indicator of future results and do Non represent returns that whatsoever investor really attained. Indexes are unmanaged, exercise not reflect management or trading fees, and one cannot invest directly in an index.

References:

Alberg, John, and Zachary Liption. "Improving Factor-Based Quantitative Investing past Forecasting Company Fundamentals." Cornell University, 2017. arxiv.org. Bailey, David H., and Marcos Lopez De Prado. "The Deflated Sharpe Ratio: Correcting for Selection Bias, Backtest Overfitting and Non-Normality."SSRN Electronic Journal, 2014. https://doi.org/10.2139/ssrn.2460551. Burkov, Andriy.The Hundred-Page Machine Learning Book. Leipzig: Andriy Burkov, 2019. Estrella, Arturo, and Frederic S. Mishkin. "The Yield Curve as a Predictor of U.Due south. Recessions."SSRN Electronic Periodical, 1996. https://doi.org/10.2139/ssrn.1001228. Glen, Stephanie. "Decision Tree vs Random Forest vs Gradient Boosting Machines: Explained Simply." Information Science Central. Accessed April nineteen, 2020. https://www.datasciencecentral.com/profiles/blogs/determination-tree-vs-random-forest-vs-boosted-trees-explained. Hoffstein, Corey. "Timing Luck and Systematic Value." Flirting with Models. Newfound Research, July 28, 2019. https://blog.thinknewfound.com/2019/07/timing-luck-and-systematic-value/. Kahneman, Daniel.Thinking, Fast and Slow. New York: Farrar, Straus and Giroux, 2015. Khillar, Sagar. "Deviation Between Bagging and Random Forest." Difference Between Similar Terms and Objects, October 18, 2019. http://www.differencebetween.net/technology/difference-between-bagging-and-random-forest/. Prado, Marcos López De. "Building Diversified Portfolios That Outperform Out of Sample."The Periodical of Portfolio Direction 42, no. four (2016): 59–69. https://doi.org/ten.3905/jpm.2016.42.4.059. Shiller, Robert. "Do Stock Prices Movement Likewise Much to Be Justified by Subsequent Changes in Dividends?" 1980. https://doi.org/x.3386/w0456 Surowiecki, James.The Wisdom of Crowds. London: Abacus, 2014. Tetlock, Philip E., and Dan Gardner.Superforecasting: the Art and Scientific discipline of Prediction. London: Random Firm Books, 2016. Yiu, Tony. "Understanding Random Forest." Medium. Towards Data Science, August xiv, 2019. https://towardsdatascience.com/understanding-random-forest-58381e0602d2. Zatloukal, Kevin. "ML & Investing Part 2: Clustering." O'Shaughnessy Asset Direction Blog & Enquiry. O'Shaughnessy Asset Management, September 2019. https://osam.com/Commentary/ml-investing-part-two-clustering.

Learn Something? Share the Knowledge!

Steven Downey is a quantitative nugget director with Holborn Avails LLC where he advises clients using a multi-cistron multi-asset class strategy. He blends all-time practices from behavioral finance, quantitative analysis, and discretionary forecasting. Working in the UAE since 2013 has afforded him the privilege to educate and help individuals from effectually the world grow their wealth. Steven and his family bask children's books, Nerf guns, and BBQs on the terrace during the COVID-19 pandemic.

0 Response to "Philip Tetlock and Daniel Gardner Superforecasting the Art and Science of Prediction 2016"

Post a Comment